Previous - Theory of Production

Cost of Production

Cost of production is the total cost for the manufacture or production of goods and services. Total cost of production is made up of fixed cost and variable cost. Fixed costs are those costs that do not vary with output and typically include rents, insurance, depreciation and set-up costs. Fixed costs are also called overhead costs. Variable costs are costs that do vary with output, and they are also called direct costs. Examples of typical variable costs include fuel, raw materials, and some labour costs.

Short Run Costs

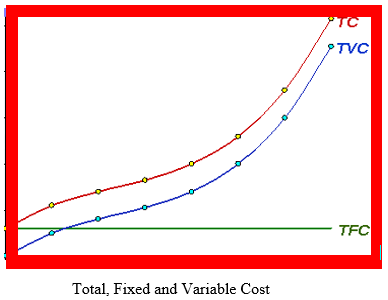

As stated above, total cost (TC) is the cost of all the productive resources used by the firm. It can be divided into two separate costs in the short run: 1) total fixed cost (TFC) and 2) total variable costs (TVC). Therefore, TC = TFC + TVC

In the following graph, notice that the shape of both the total cost and variable costs curves is the same only that the total cost curve is higher than the variable cost curve because of the inclusion of fixed cost in total cost. In addition, it can be noticed that fixed cost curve is a straight horizontal line representing the fact that it remains the same when output changes. Even if output falls, fixed cost will also remain the same because such costs are fixed in nature.

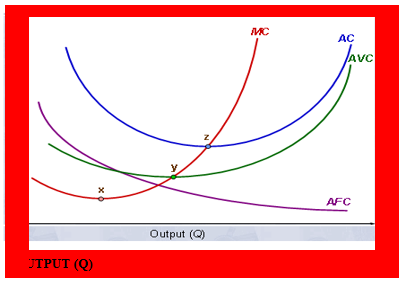

Average costs are different from total costs. There are three types of average costs which are average total cost, average fixed costs and average variable costs. Average fixed costs are found by dividing total fixed costs by output. Average variable costs are found by dividing total variable costs by output. Similarly, average total costs are found by dividing total costs by output.

Notice that unlike total fixed costs, average fixed costs falls as can be seen in the following graph. This is so because average fixed costs are determined by dividing total fixed costs by output; the numerator which is total fixed costs remains unchanged but the denominator which is output rises throughout.

Marginal Cost (MC) is the change in total cost resulting from a one-unit change in output. This is also U-shaped.

Long Run Costs

Long run production costs include all costs after plant and industry size are allowed to change (expand or contract). The long run ATC curve shows the least cost per unit at which any output can be produced after the firm has had time to make all appropriate adjustments in its resources. In long run cost, the issue of economies of scale arises.

Economies and Diseconomies of Scale

Economies of scale are related to and can easily be confused with the notion of returns to scale. Where economies of scale refer to the relationship between a firm's costs and output, returns to scale describe the relationship between inputs and outputs in a long-run (all inputs variable) production function. A production function has constant returns to scale if when an input is increased by 1 unit, output will increase by the same proportion. Decreasing returns to scale is when input in increased by 1 unit, output will increase by less than 1 unit. Increasing returns to scale is when input is increased by 1 unit, output will increase by more than 1 unit.

Economies of scale show a different relationship which is the relationship between cost and inputs. Economies of scale explain the relationship between the long run average cost and the production of a unit of good; in this case average cost will be decreasing with increases in output. On the other hand, diseconomies of scale explain the relationship between the long run average cost and output when average cost is increasing with increases in output.