Previous - Microeconomics Topics

Definition of Economics

Economics is the social science that studies how consumers, firms and the governments make choices on allocating scarce resources to satisfy the unlimited wants of society. Economics is divided into two broad categories which are microeconomics and macroeconomics. Microeconomics deals with individual agents such as consumers, firms and state-owned companies. Macroeconomics deals with the aggregate or the entire economy and focuses on issues such as aggregate demand and aggregate supply, inflation, unemployment, the exchange rate, international trade and foreign reserves.

The Three Basic Economic Questions

The three fundamental questions in economics are:

-

What to produce?

In economics, what to produce is usually determined by the demand for goods and services by consumers. Therefore, what consumers demand is what is usually produced. The decision as to what to produce is also influenced by the type of economy; whether the economy is a planned or command economy, a free economy or whether the economy is a mixed economy. In a planned or command economy, what to produce is determined by a central economic authority established by the government. In a true free market, what to produce is determined by choices of consumers. However, most nations fall somewhere between a true command economy and a true free market system and production is determined by both the demand by buyers and by some level of government intervention.

-

How to produce?

Many different ways and methods are available to firms in determining how goods and services can be produced. A firm can employ a few skilled or a great deal of unskilled workers. The firm can also be more capital intensive with high technological methods of production. The firm can also produce locally or overseas. In addition, firms can use new or recycled raw materials to make their products. These are some of the issues that can confront firms in the economy regarding how to produce society’s goods and services.

-

For whom to produce?

If a good or service is produced, a decision must be made as to who will consume it. Decisions to have one person or group receive a good or service usually means it will not be available to others or less will be available to others. Usually those persons or groups in society who and which have access to financial capital will usually have quicker access to the goods and services produced by society. Therefore, the question as to whom to produce for is usually geared to those persons in society who have the financial capacity and can afford to purchase these goods and services that are produced.

Scarcity, Choice and the Concept of Opportunity Cost

Scarcity occurs since resources are limited but wants are unlimited. Economic wants are defined as desires that can be satisfied by consuming or utilizing a good or service. Due to the fact that resources are limited, consumers cannot have all the goods and services they want. Consequently, these consumers must choose some goods and services and give up others. There is a difference though between wants and needs. Wants are goods or services that are not necessary but are desired by consumers. Needs are defined as goods or services that are required and considered necessary. This would include the needs for food, clothing, shelter and health care. Choice must therefore be made between competing options or a decision must be made.

Central Economic Problem

Human wants are unlimited but resources are limited. This is where concept of scarcity arises. The law of scarcity states that wants always exceed society’s ability to meet them. This will mean that every society faces the economic problem of choosing what to produce, how to produce society’s desired goods and for whom to produce. Therefore, in order to get more of a good, more of another has to be given up which leads to the concept of opportunity cost. Opportunity cost is expressed as the relative cost of one alternative in terms of the next best alternative. Therefore, the central economic problem is how society makes the best use of its limited or scarce resources to satisfy its unlimited wants.

Production-Possibilities and Opportunity Cost

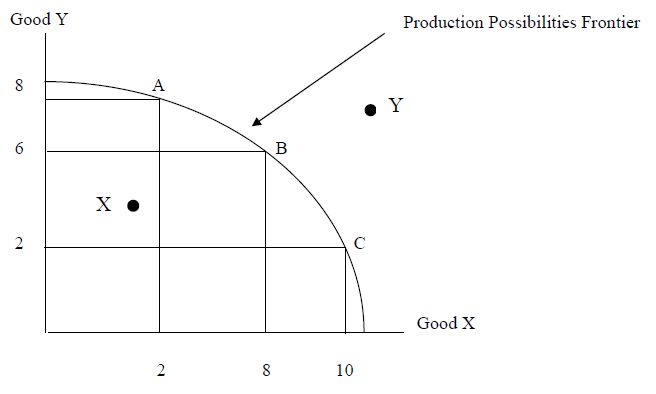

Scarcity can be illustrated by the use of the Production Possibilities Frontier (PPF) which shows all the possible combinations of output that can be produced when resources are fully employed. It shows the opportunity cost of producing a good.

An illustration of the PPF is provided in the following graph. Points on the PPF such as A, B, and C are attainable by the economy and are efficient. Points beyond the PPF such as Y, are not attainable due to scarcity of resources. Points within the PPF such as X, are attainable but are inefficient since they occur when resources are not fully employed or where there is either unemployed resources or when resources are inefficiently allocated. Efficiency requires the full employment of all resources. According to the PPF, points A, B and C are all on the frontier and represent points of efficiency. If the economy is producing at point A, in order for the economy to produce 6 more units of Good X (from 2 units to 8 units), it must give up 2 units of Good Y (8 units to 6 units). This can be shown as a movement from point A to point B.

The opportunity cost of producing the 6 extra units of Good X will therefore be the amount of Good Y that was given up in order to get more of Good X which is the 2 units of Good Y foregone. Opportunity cost is expressed in relative terms in the sense of one alternative relative to the other alternative. If we want to produce even more of Good X, we will have to give up more and more of Good Y. In addition, the opportunity cost of producing 2 more units of Good X (from 8 to 10) is the 4 more units of Good Y (from 6 to 2) that must be given up; this is shown as a movement from point B to point C along the PPF.